BY:

SHARE:

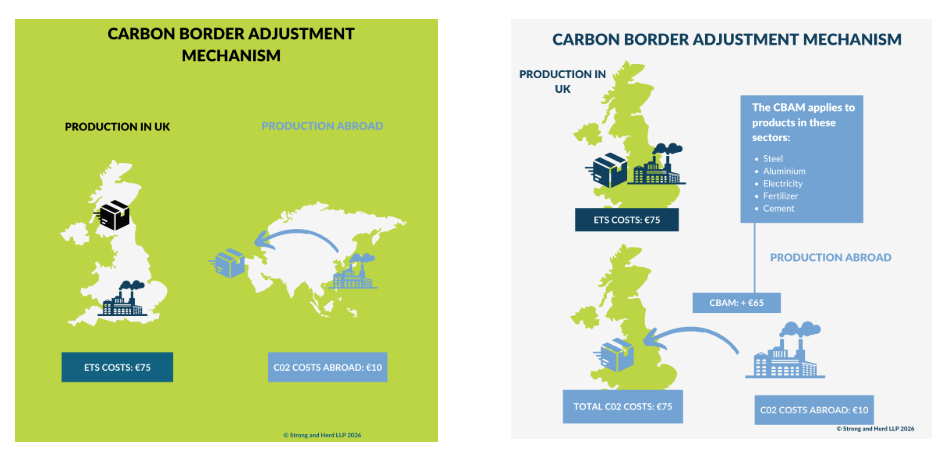

The UK Carbon Border Adjustment Mechanism (UK CBAM) is a forthcoming measure designed to reduce carbon leakage by applying a carbon-related charge to certain carbon-intensive goods imported into the UK. It mirrors the policy intent of the EU CBAM, ensuring imported goods face a comparable carbon cost to goods produced domestically while operating within the UK tax system.

In practical terms, CBAM is intended to prevent a shift of production (and associated emissions) to jurisdictions with less stringent climate policies, and to support fair competition between domestic producers and importers.

While the UK CBAM shares core concepts with the EU model, it will operate differently in several areas. Importers of in-scope goods should therefore understand how the UK rules will apply to their supply chains, data collection, and compliance processes.

The UK CBAM sits within HM Treasury’s remit under the Finance Act and is expected to operate as a tax. With implementation scheduled from January 2027, businesses importing potentially in-scope goods should confirm their classification and prepare for registration, reporting and payment obligations ahead of go-live.

How the UK CBAM rules are being developed

CBAM legislation and guidance are being developed in stages, including primary legislation (setting the framework) and secondary legislation and notices (setting out operational detail). Importers should monitor published updates as the draft regulations are finalised.

- Primary legislation: introduced in the Finance Act 2026 (see the UK Parliament website for the Act and associated documents).

- Secondary legislation: draft secondary legislation has been released in two stages for technical consultation, alongside draft notices intended to have the force of law. The first set was published on 10 February 2026 for a 6-week consultation, which closed at 11:59 pm on 24 March 2026. The second set was published on 9 April 2026 for a 6-week consultation and includes the system boundaries document and force-of-law notices; this consultation closes at 11:59 pm on 21 May 2026.

The UK CBAM will apply to certain goods imported into the UK in the following sectors:

- Aluminium

- Cement

- Fertiliser

- Hydrogen

- Iron

- Steel

Not all goods within these sectors are in scope. Importers should use the commodity codes listed in Annex B to confirm whether a product is covered.

The government expects to keep the list of in-scope goods under review and may update the scope over time.

Annex B: Commodity codes within the scope of CBAM

The definitive scope check is by commodity code. Importers should use the published annex listing the commodity codes within the scope of CBAM (referred to as Annex B in the policy summary) when assessing whether particular products are covered.

Who is responsible for UK CBAM?

Liability generally sits with the person making the Customs Declaration, or the person on whose behalf the declaration is made—i.e., the importer.

As the UK CBAM is expected to operate as a tax, the liable person will need to register with HM Revenue & Customs (HMRC) and account for in-scope goods that pass the tax point during each accounting period.

Importing CBAM goods

If you import goods that may be in scope, start by confirming classification against Annex B (commodity codes). You must register for UK CBAM with HMRC if the value of in-scope goods imported over the preceding 12-month period or expected to be imported over the coming 30 days exceeds the £50,000 minimum registration threshold for the relevant period.

If you become liable, you will generally have 30 days to register with HMRC. The government has indicated that transitional arrangements may apply in the first year to provide additional time to register.

UK CBAM will be accounted for over defined accounting periods, with payments generally due around two months after the end of each period. As the regime is implemented, businesses should track HMRC guidance for confirmation of the accounting-period cycle, submission requirements, and detailed deadlines from January 2027.

Registration is expected to be completed via the liable person’s Government Gateway account; the service is not yet available. In the meantime, importers can use the lead time to confirm organisational readiness (who will register, who will report, and what data will be required).

Accounting periods, returns, payments, and repayments

UK CBAM will be operated through defined accounting periods with associated return and payment processes and may also provide for repayments in certain circumstances. Importers should refer to the final secondary legislation and HMRC guidance for the confirmed accounting-period cycle, what must be included in returns, payment and repayment rules, and the applicable deadlines.

HMRC is hosting webinars on 7 May regarding the draft secondary legislation.

Draft secondary legislation: consultation and webinars

- 7th May 2026 09:30 – 10:30 (BST) Sign up here

- 7th May 2026 15:00 – 16:00 (BST) Sign up here

The consultation period for the draft legislation is open until May 21st, 2026 - https://www.gov.uk/government/consultations/draft-regulations-carbon-border-adjustment-mechanism-cbam-emissions-and-verification

OneCall™ Email assistance as and when required; A one-call solution for all your import, export and customs enquiries. Export help. Import help. Customs help.

Stay informed about customs and international trade matters by subscribing to our OneCall™ service. This comprehensive offering includes a dedicated email helpline for support, timely practical updates direct to your inbox (Did You Know?), monthly UK Customs & Trade Briefings and access to an interactive members' area with an exclusive community for our subscribers.

International Trade Updates & Spotlight Newsletter

Subscribe to our free information emails covering international trade topics...

MORE INDUSTRY INSIGHTS...